ALL INDIA UNION BANK RETIREES’ FEDERATION

(Affiliated to All India Bank Retirees’ Federation)

A/12, Girdhar Apt., Kastur Park, Shimpoli Road, Borivali (W), Mumbai 400 092

Chairman President General Secretary

D. A. Masdekar B. G. Raithatha R. K. Powar

9970899393 9427207021 7710030963

|

20th August 2017

N O T I C E

NOTICE is hereby given that the Central Committee meeting of All India Union Bank Retirees’ Federation will be held on the 16th and 17th September 2017 at 10.30 a.m. at Hotel Syona Residency, Behind Charbagh Bus Stand, Lucknow to transact the following business:

A G E N D A

- To co-opt 2 additional Office Bearers to AIUBRF as agreed by senior Office-bearers & CC members in Nagpur on 25th September 2016;

- To approve amendment to Clause No. 9 of the Constitution:- Nomination of maximum 15 Central Committee members (including officer-bearers) of each state affiliate, subject to 1 committee member for every block of 100 members of the Basic Unit, but not exceeding 15 from any state and at least 1 from each state Unit;

- To read and confirm the minutes of the Central Committee meeting held on 17th September 2016;

- To present and discuss the General Secretary’s Report on the activities of AIUBRF, AIBRF and other issues mentioned in the Report;

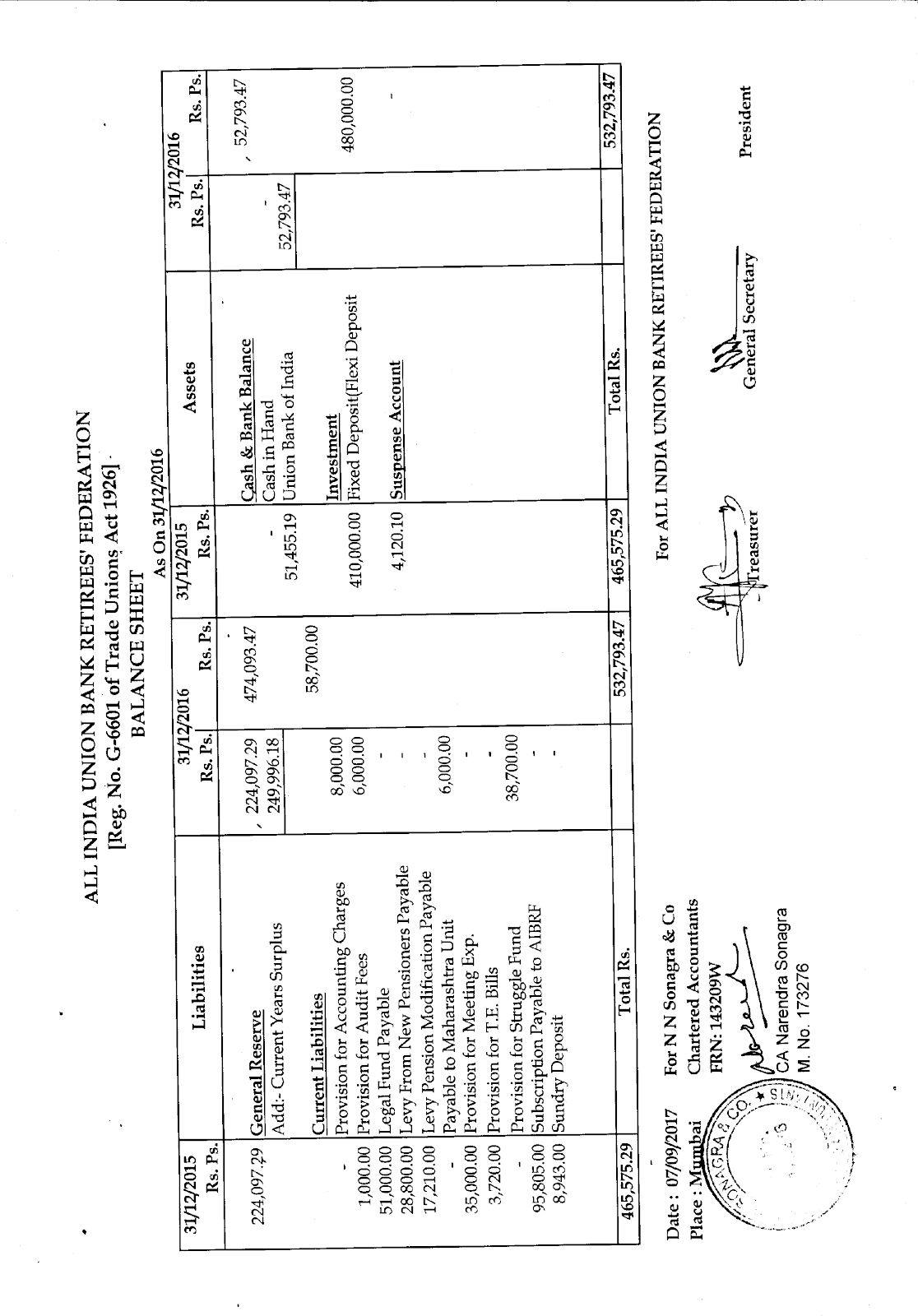

- To approve the Audited Statement of Accounts for the year ended 31/12/2016;

- To discuss about the dues of Subscription Fee by State Units to AIUBRF upto December 2016, and outstanding Struggle Fund contribution to AIBRF by Units as of 31/12/2014;

- To decide the issue of affiliation of State Units of AIUBRF to the State-wise Units of AIBRF;

- Any other matter with the permission of the Chair.

(R. K. Powar)

General Secretary

Minutes of the Central Committee meeting held at Nasik on 17th September 2016

In terms of Notice and intimation, the Central Committee meeting of the Federation was held at Aurangabadkar Hall, Nasik on 17th September 2016 to transact the following business:

A G E N D A

- Confirmation of Minutes of the last CC meeting held at Indore on 08th and 09th October 2015;

- Approval of General Secretary’s Report for the entire current term, to be presented in the General Body meeting;

- Approval of Financial Statements of the Federation’s accounts from 01/01/2013 to 31/08/2016;

- Approval of proposed Resolutions (if any)

- Any other matter with the permission of the Chair.

Shri. D. A. Masdekar, President, presided over the meeting. He read out the Notice and requested the General Secretary to take up agenda number 1 of the meeting.

Shri. Pratap Shukla, General Secretary, presented the copy of the Minutes of the last Central Committee meeting held on 8th& 9th October 2015, which was unanimously passed.

After passing the last CC meeting’s Minutes, the General Secretary of the Federation presented his report for the operative period, for perusal and approval of the CC members. After reading the details of GS report, CC members expressed their reactions on various points of the report.

Many members effectively participated in the discussions on points mentioned in the Report. Few members expressed satisfaction over AIBRF’s action programmes chalked out for achieving major economic demands such as 100% DA neutralisation to pre-Nov 2002 retired employees, increase in existing rate of Family Pension to fall in line with RBI pension scheme, Updation of Pension; and appreciated AIUBRF and its State Units’ participation. Although the authorities concerned so far did not accede to the above legitimate demands of the retired employees, the members opined that AIBRF should continue the action programs to draw the attention of IBA and Ministry of Finance and also pursue the legal actions already initiated by some of the affiliates of AIBRF.

The members also expressed fear about the likely increase in the premium of Medical Insurance Scheme for 2016-2017 because of steep increase in the claim ratios as reported. Members opined that the Medical Insurance Scheme was a welcome step in view of some of the important features such as pre-ailment is allowed, no age limit factor etc., but substantial increase in premium amount as contemplated might put financial burden, more particularly on the Family Pensioners as well as some of the award pensioners whose monthly pension is less than Rs. 10,000/-. There was consensus that AIUBRF should take up the matter with management to prevail upon IBA/UIIC not to enhance the premium of insurance in the second year.

Members also said that the bank management repeatedly fail to communicate directly with the retired employees due to which many retirees remain unaware of the decisions &/or scheme/s available for the benefit of the retired employees. It was also reported that information displayed on the web page reserved for the retirees is also not updated periodically. Members suggested that AIUBRF should inform the management to ensure that the retired employees are informed either by sms or emails.

Few of the members have suggested that the settlement of claims under UBIREMAS is delayed on account of improper approach adopted by various Regional Offices. It is also reported that the personnel of staff section of Regional Offices advice the retirees to claim the medical bills by submitting the claims to UIIC. Members opined that the management should not insist to submit claims / bills to insurance company.

There was general feeling that the bank management should provide some amount of subsidy out of the funds of UBIREMAS as has been done in other nationalised banks. It is suggested that AIUBRF should pursue the matter for favourable decision in the matter.

Many members said that the issues of the retired employees are not resolved in time causing lot of hardships to them. It is also reported that in many cases, the management at RO/FGMO do not respond to the representations of retired employees.

Our Bank is paying Leave Encashment to the Officers compulsorily retired on or after 30th April, ’15. The members stated that after taking further permission of IBA the following Banks have taken decision to pay leave encashment to the officers compulsorily retired on any day after 27th November, 2000.

- UCO Bank

- Syndicate Bank

- Bank of Baroda

- Punjab National Bank

Members desired that AIUBRF should take steps to convince our Bank’s management to approve the payment of leave encashment to these officers as has been approved in the above four Banks.

On the organisational matters, members said AIUBRF should play a major role to mobilize the retired employees on all India bases. Members suggested chalking out the programme to bring back those States left affiliation of AIUBRF. Members further said that many issues of retirees remain either unattended or not resolved for long period and therefore, the leadership must take immediately steps to ensure that the management disposes the cases early.

The members deliberated on the General Secretary’s report and approved the same to be presented in the conference.

Thereafter the agenda for approval of financial statements of the Federations’ accounts from 01/01/2013 to 31/08/2016 was taken up by the Treasurer of Federation and the accounts were approved and passed by the Central Committee Members unanimously.

The next agenda on adopting the resolutions was discussed and it was agreed by the house to adopt the resolutions on the lines of the AIBRF’s demands.

As no other matter had come up for discussion, the President declared the meeting as concluded.

General Secretary

(R. K. Powar)

Minutes confirmed on _________________

(B. G. Raithatha)

President

GENERAL SECRETARY’S REPORT

Dear Friends,

This is the first Central Committee meeting of the new team of office-bearers and central committee members convened after our 5th Triennial Conference held in September 2016 at Nasik, Maharashtra. The Presidium welcomes all of you on this occasion to the historic city Lucknow.

I have endeavored to include the important events occurred, since our 5th Triennial conference held in September 2016, in the banking sector, the government and RBI combine’s approach for merger &/or consolidation of public sector banks, the on-going negotiations on new wage structure/allowances for the existing employees of the banks and seeking improvement in retirement benefits including Pension similar to RBI/Central Government including past retired employees, follow up of Record Note dated 25/05/2015, extension of erstwhile Pension Scheme in banks in lieu of NPS, existing medical insurance scheme and the scheme of Top-up facility as envisaged by AIBRF and also by insurance companies, 100% DA neutralization for pre-Nov 2002 retired employees, increase in Family Pension, etc., and reporting on the activities of AIUBRF and AIBRF.

I welcome your suggestions and additions to this report during the discussions, if any event is not dealt with, &/or amendments/modifications.

- OBITUARY :

During the period of the Report, many eminent dignitaries, political leaders, Trade Union leaders, activists in various walks of life and few members of our State Associations passed away. We place on record our sincere condolences at their sad demise. I request the house to observe a minute’s silence in their memory.

- POLITICAL DEVELOPMENTS :

AIUBRF does not support or follow any ideology or any political party, but we cannot remain distant from the developments in the political arena of our country, and as citizens, should remain alert to attempts to fragment society or create divisiveness to the country. We need to support the constitution of our country, including the Fundamental Principles that form the unwritten basis of our social, secular framework, in true spirit and perspective.

- ECONOMIC DEVELOPMENTS:

A strong, efficient and corruption free administration is essential for successful economic growth. India has the potential to grow like a developed economy if the government is able to meet the plans not only on papers but in reality. There is a need of constant surveillance of plans to get the best result and for better development in the future.

The Indian economy is expected to grow by 7.2 per cent F Y 2017-18 as per the forecast by International Monetary Fund.

In the Union Budget 2017-18, the major push of the budget proposals was on growth stimulation, providing relief to the middle class, providing affordable housing, curbing black money, digitalization of the economy, enhancing transparency in political funding and simplifying the tax administration in the country.

It is believed that GST would lead to higher tax collection, greater digital financial inclusion and make India’s fundamentals stronger and yet not increase the burden on the poor. Given the efficiency and revenue gains that the reform will eventually achieve, the overall impact of the GST on equity and poverty is likely to be positive.

Economic growth and development is essential for best utilization of resources, economic welfare, and sustainability. Economic growth ought to improve citizens’ living standards.

- INDIAN BANKING SECTOR:

The Indian banking system consists of 26 public sector banks, 25 private sector banks, 43 foreign banks, 56 regional rural banks, 1,589 urban cooperative banks and 93,550 rural cooperative banks, in addition to cooperative credit institutions. Public-sector banks’ control have reduced to less than 60 per cent of the market, thereby creating a larger market share for private Banks than in the past. Technological change in Banks has caused many changes, bringing in 60% banking thru alternate channels like internet banking, ATM, and also the concept of self-banking in Union Bank branches called 'Utkarsh'. Banks are also now encouraging their customers to make transactions by use of mobile phones.

The government and Reserve Bank of India are in talks to shore up public sector banks capital in time bound manner due to the high provisioning burden.

Public Sector banks require capital mainly because of a sharp rise in non-performing assets (NPAs) in the last decade due to delays in repayments from sectors like power, steel and infrastructure.

The RBI blamed lenders for the mess, saying their poor credit appraisal systems have led to the pile of bad loans, which tops over Rs. 9 trillion now. Gross NPAs of the banking system have risen to 9.6% as of March 2017. Taken together with the loans that have been restructured the ratio of stressed rises to 12% of total banking sector loans. 86.5% of gross NPAs are accounted by large borrowers which are defined as borrowers with aggregate exposure of Rs. 5 Crore and above. The regulatory or rather the economic challenge in dealing with the issue gets accentuated when seen against the capital position of some of the banks particularly public sector banks; that six public sector banks have been put on the so-called prompt corrective action (PCA) so far, this year.

Bank of Maharashtra, Central Bank of India, IDBI Bank, Dena Bank, United Bank of India, Allahabad Bank and Indian Overseas Bank have been put under watch by the RBI due to rising NPAs and erosion of capital. PCA action by the RBI has resulted in certain restrictions in lending and expansion till the capital position of these banks improve.

There are various estimates on the capital requirement of public sector banks. According to the latest report in June, Indian public sector banks require between Rs. 70,000 Crore to Rs. 95,000 Crore of capital approximately five times the Rs. 20,000 Crore budgeted by the government towards capital infusion until March 2019.

- NON PERFORMING ASSETS:

Banks NPAs have almost doubled in the last 2 years largely due to the classification requirement of the RBI. Demonetization stalled the recovery process further. Gross bad loans at commercial banks increase to 9.6 per cent of total advances by March 2017, from 7.6 per cent in March 2016.

The RBI said a total of 46.54 lakh cases to recover NPAs were filed in Lok Adalats, Debt Recovery Tribunals and under the SARFAESI Act.

According to CARE Ratings’ analysis of the first quarter results June 2017 of 38 banks; IDBI Bank (with gross NPA ratio of 24.11 per cent of gross advances) and Indian Overseas Bank (23.6 per cent) have NPA ratios of over 20 per cent. Among PSBs, Indian Bank has the lowest GNPA ratio of 7.21 per cent.

Eight PSBs banks — IDBI Bank, Indian Overseas Bank, UCO Bank, Bank of Maharashtra, Central Bank of India, Dena Bank, United Bank of India, and Corporation Bank — had a GNPA ratio of over 15 per cent as of June 2017.

YES Bank is the only bank in the sample of 38 banks with a GNPA ratio of less than 1.

State Bank of India (SBI) accounted for the largest share of about 22.7 per cent (or Rs.1,88,068 crore) in the total NPAs of 38 banks (aggregating Rs.8,29,338 crore) as of June-end 2017.

SBI, Punjab National Bank, Bank of India, IDBI Bank, and Bank of Baroda accounted for 47.4 per cent (totalling Rs.3,93,154 crore) in the total NPAs as of June-end 2017.

Among the top 20 banks, according to GNPAs in absolute terms, 18 are PSBs and only two are private sector banks — ICICI Bank and Axis Bank. These two private sector banks have a combined share of 7.9 per cent in total NPAs.

In the April-June quarter (Q1) of FY17-18, NPAs of a sample of 38 banks increased by a sharp 34.2 per cent on a year-on-year basis. Also, the NPA ratio increased to 10.21 per cent in June 2017 from 8.42 per cent in June 2016, which is the highest in the last six quarters.

On a quarter-on-quarter basis, the increase in NPAs has been the highest in Q1 of the financial year 2017-18 witnessing an increase of about 16.6 per cent to reach ₹8,29,338 crore as of June 2017.

The government has taken initiative to improve the recovery of bank loans, IBC (Insolvency and Bankruptcy Code) has been enacted and SARFAESI (Securitization and Reconstruction of Financial Assets and Enforcement of Security Interest) Act and RDDBFI (Recovery of Debts due to Banks and Financial Institutions) have been amended. Further, six new Debt Recovery Tribunals (DRTs) have been established for improving recovery.

Much is talked about and assured by the Government in respect of initiatives to speed up the recovery of NPAs, but the success of these initiatives will depend upon the inclination of the large corporate borrowers to pay the dues of the banks. It is also hoped that the measures put in by the Govt/RBI will not lead to huge 'haircuts' to the detriment of the Banks.

- FARM LOAN WAIVERS:

The UP government’s waiver of farmer loans, dramatic protests by Tamil Nadu farmers in Delhi, followed by pressure of opposition political parties compelling Maharashtra Government to waive farm loans and a warning from the RBI Governor against loan waivers — have once again brought farm loan write offs under public glare.

The Centre or States take over the liability of farmers and repay the banks. Waivers are usually selective — only certain loan types, categories of farmers or loan sources may qualify. Farm loan waivers are at best a temporary solution and entail a moral hazard — even those who can afford to pay may not, in the expectation of a waiver. Such measures can erode credit discipline and may make banks wary of lending to farmers in the future. It also makes a sharp dent in the finances of the government to write-off.

Though the composition of Farm Loan waiver may be around 2% of the total NPAs, loan waivers cost tax payers. The larger worry is that these costs may not be one-off, as politicians may wave this carrot to win elections.

There are no two opinions that loan waivers add to the already elevated non-performing assets of banks. It is also a fact that the magic wand of a waiver can offer temporary relief, but long-term solutions are needed to solve farmer woes.

- MERGERS & CONSOLIDATION OF PUBLIC SECTOR BANKS:

The merger of Associate Banks of SBI with State Bank of India has completed a task proposed a few years ago, that was initiated by merging of 2 other associate Banks, State Bank of Indore and State Bank of Saurashtra into SBI. Despite the appeals and protests of employees, the merger of the remaining Banks of SBM, SBT, SBH, and SBBJ into SBI became a reality on the 1st April 2017, into the large Banking conglomerate in India. The process of rationalisation of staff and branch offices have also begun, and 3500 employees of the associate banks took the offered VRS scheme.

In the third week of August 2017 the union cabinet has given approval to the framework for consolidation of public sector banks. It is gathered that the cabinet approval for consolidation came in the face of banking operations across the country being hit on 22/08/2017 as over 10 lakh bank employees in more than 1,30,000 branches pan-India struck work protesting against reforms in the banking sector, including proposals of merger of state-run banks.

The decision taken at the Cabinet meeting saying this could reduce PSB’s dependence on government for capital. The cabinet approved the constitution of an alternate mechanism that will oversee proposals with regard to consolidation of banks, which should come from the public sector banks; meaning if any PSB board gives a consolidation proposal, to oversee that proposal an alternative mechanism i.e. constitution of committee of ministers, will be in place to give “in principle” approval for the proposal of the banks for a scheme of merger/amalgamation.

The government has said that the aim of consolidation is to create strong and competitive banks based on commercial considerations and the ability to absorb market shocks.

As in the merger in SBI, proposals to phase out of the employees, the reduction of branches and the ‘cost rationalization’ of the excesses are widely anticipated. Whether this action of the government in merging Banks into larger entities will create the impetus in Banking that the advisors believe will happen, remains to be seen.

But this appears just another step on the roadmap to de-nationalise the Public sector Banking sector and bring in market oriented private Banks. It is pertinent to point out, that VRS has been offered to the employees, and those availing VRS out of fear of change in working, transfer, redundancy of career paths etc. are likely to join the retirees Associations in their respective Banks. Even the character of the Retirees Associations will undergo a change with the multiple effects of several retirees’ Unions coming under a common umbrella. Hence the challenges of this merger/consolidation of public sector banks will be seen in retirees too. The issue is an agenda before our apex body AIBRF in its forthcoming meeting/s.

- MOU WITH UNIONS/ASSOCIATIONS:

As a first step towards infusing the additional capital and moving to the merging of Nationalized Banks, the government has insisted on 10 Banks that were showing losses in the last 2 quarters of the financial year 2016-17, were called upon to sign MOUs with their respective Unions for capital infusion by the Government towards meeting CAR level on account of credit expansion projected by the banks for the next fiscal. The condition is that the Bank Management and the Unions/Associations should sign an MOU to commit to achieve certain parameters in certain broad areas as a turnaround package as decided by the Ministry, and the finer points of these parameters in terms of measurable and quantifiable factors will be worked out by SBI Cap.

The details of the MOU are as follows, but not limited to just the following areas

- Asset quality including recovery, NPA reduction etc;

- Optimum utilization of capital, sale of non-core assets, broad basing investor base, etc.,

- Improvement in productivity/efficiency including branch rationalization;

- Improvement in business processes (BPR);

- HR Policies and Practices

However, this is the first time where commitment from employees and officers and its Unions and Associations is sought in writing to take the responsibility of successful implementation of the turnaround plan. The MOU also lays down that a committee comprising of the senior management of the bank, i.e. CMD & EDs, and representatives of the Officers’ Associations and Employees’ Unions will monitor the implementation of the turnaround plan on a monthly basis. This is despite the fact that representatives of officers and employees on the Boards of banks have been kept vacant for the past 2/3 years, and are not being filled up in accordance with the rules for the same under the Bank Nationalization Act.

How the Unions and Associations are expected to play a role by signing an MOU for the resurgence of Banks, is a big question. If the regulators require banks to meet their CAR levels, this can only be done by either increasing capital, or not expanding credit. Non expansion of credit therefore becomes a business decision, albeit a forced one by regulation.

It is incomprehensible as to how the Unions and Associations are capable of influencing any of the above decisions, hence the “threat” by the Government to withhold capital unless the MOU was signed by the Unions and Associations should be seen through for what it is – a crude attempt to railroad the Unions/Associations into signing an MOU that covers the relevant aspect of Unions/Associations activity.

Needless to underscore, that Unions and Associations have been alive to the problems of Banks development over many years, and it did not need any MOU to threaten Bank employees into putting in their best to improve the banks position in productivity and efficiency. And the threat of withholding capital from Banks if such MOU is not signed by Unions/Associations is clearly without logic or reason. It can be interpreted as a step of coercion of the Unions and Associations leadership by the Government towards implementing plans for the banks to reduce work force, with a long term goal of merger and privatisation.

In addition the threat to withholding of benefits, which may also include the forthcoming wage revision of bank employees and officers, this move has a very sinister feeling, and will surely affect the retirees as well.

It is suggested that members remain alert to the happenings on the issue of MOU and proposed mergers/consolidation of Nationalized Banks, as our interests are most certainly committed by its outcome in the future.

- MOU IN OUR BANK:

As stated in the preceding para, the government insisted the Bank managements and the Union/Associations, which were showing loses in the last 2 quarters, to sign an MOU to commit to achieve certain parameters as a turnaround package.

For allocation of capital, the Government has attached the condition of obtainment of MOU to be signed by Unions/Associations on similar lines as had been obtained in other 10 Banks. Our Bank took up the issue with the Government to not to insist for MOU as our bank is a profit making Bank and no turnaround programme is applicable to it. However government did not accede to Bank’s request. There after the matter was placed before the Bank’s Board on 22nd March 2017 where the Board also discussed the matter and accordingly directed the Management to once again represent to Government to release capital without insisting for MOU. However the government did not agree to it and insisted for MOU.

In the joint meeting of management, Union & Association convened for signing MOU, Bank explained the development, its efforts with the government, other avenues of raising capital & its limitations, no possibility of going for Rights issue but the dire need for capital for further expansion. Bank had also expressed its frustration over the Government’s unyielding stance and its inability to differentiate between performing & non Performing Banks.

The union/association leadership explained the bank management that only policy changes from the Government can alone bring turnaround of the Industry and was able to get the following assurance/commitment from the bank management.

The union/association leadership explained the bank management that only policy changes from the Government can alone bring turnaround of the Industry and was able to get the following assurance/commitment from the bank management.

- Union Bank MOU envisages for improving its performance; thus the purpose and object of MOU have been clearly and distinctly made different.

- MOU allows the Bank to adapt to all kinds of resource mobilization and lending as it was doing till now. No restriction is imposed on business making.

- In the last year the cost to income ratio has come down by near 6%. However MOU projects to reduce the cost to income ratio by 3% in next three years at reduction of 1% every year. Such reduction is not by curtailing expenses but through increase of income that is projected at reasonably achievable rate. This will enable the Bank to meet its operational expenses arising out of expansion etc.

- No curtailment for recruitment and Bank is permitted to go for recruitment to meet its need that will include natural wastages and expansion. Bank will recruit in the future to ensure that total number of employees in next 3 years is increased from 36877 as at 31st March 2017 to 38688 in March 2020. Such projections have been made by factoring the increase in number of outlets, new activities, usage of alternate channels, technological innovations and other expansion.

- The Employee expenses for next 3 years have been projected by taking in to account average increase on account of normal increments and other benefits, inflation, and the wage revision rise. Thus ensured no compromise in staff benefits and staff welfares.

- Bank will reserve its right to open branches but by taking in to account the digitalization and government’s directions on cash less economy. It was decided that Bank will expand every year with number of branches at 0.5% of number of branches at the end of previous year. Besides it is also decided to relocate our existing branches to new locations to leverage its further growth.

- Bank will not dispose of its non- core investment. This means that Bank will not sell its non-core investment to raise capital but confident of raising capital from the government and / or from market.

- 260 are loss making branches out of which 22 are loss making for the last 5 years. Bank will ensure turn round of these branches or for rural and semi urban branches the Bank will relocate or close with the consent of the district authorities.

- Bank has already Board approved plan to raise capital through market issue or issue of shares to government.

- The projections in 1) arresting slippages 2) recovery & gradation been made keeping in view the conditions of accounts, availability of assets, market conditions and other factors connected to it. Even sale of NPA to ARCs will be minimal but as per Bank’s policy ensuring no loss to the Bank.

- Over all projections of the Bank in all parameters and in all areas are in sync with the business plan figures decided.

- There will be committee consisting of representatives of majority Union/Association and Top Management to decide strategies and implement & monitor the same.

With the assurance of the bank management, the majority Union/Association of employees and officers have signed MOU on 29th March 2017 and 2nd MOU on 29th June 2017.

It may please be noted that the in-service majority Union & Association have taken utmost care to protect the interest of the employees and officers, thereby also taken a pragmatic approach to safeguard the interest of the retired employees to continue the receive the benefits from our bank as availed hitherto.

AIUBRF records with appreciation the steps taken by the in-service leadership to prevail upon the bank management to commit unequivocally the objects of the MOU signed on 29th March 2017 and 2nd MOU on 29th June 2017.

- ENHANCEMENT OF GRATUITY CEILING:

The Government has approved the pay panel recommendations of doubling ceiling of gratuity from Rs. 10.00 lakh to Rs. 20.00 lakh to the Central government employees with effect from 01/01/2016, but has not taken any decision on the effective date of payment to financial sector employees, which is causing discord even among our retiree members who have retired over a year ago.

The banks are paying the gratuity amount to the retired employees as per Payment of Gratuity Act 1972. The Central Cabinet has approved the enhancement in gratuity amount hike in the gratuity amount of Rs. 10.00 lakh to Rs. 20.00 lakh subject to Parliament nod. The details of the recommendations are not known; hence we do not know the effective date of implementation of the revised gratuity amount to the bank employees.

- MANAGEMENT OF PENSION FUND:

Our Pension Scheme is “defined benefit pension” where the benefits are not directly connected / dependent on performance of Pension Fund. The future improvements depend on performance of Pension Fund created in our bank for this purpose. It is our responsibility to ensure that Pension Fund is effectively managed by the Trustees as per provisions and spirit of the Pension Regulations, 1995.

We understand that the financial position of the Fund as on 31st March 2016 with comparative figures of March 2015 is as under:

(Rs. In crore)

Item Under Liability

|

2016

|

2015

|

Item under Asset

|

2016

|

2015

|

Item Under PL

|

2016

|

2015

|

Pension Fund

|

8469

|

7167

|

Investment

|

8937

|

7675

|

Interest earned

|

814

|

577

|

Surplus

|

813

|

566

|

Cash &Bank Bal

|

345

|

58

|

Exp

|

0.37

|

11

|

- The Bank has made total contribution of Rs 1413.35 cr to pension fund in 2015-16 compare to Rs 1366.55 cr in the previous year.

- The pension fund has a surplus of Income over Expenditure of Rs 814 cr and the same is sufficient to cover the yearly pension outgo of Rs 680.71 cr. Thus the Pension Fund has a net surplus of Rs. 132.83 Cr after meeting the total pension payments besides keeping the corpus intact.

- Under portfolio management with LIC as the Fund Manager the Pension fund has investment of Rs. 3621.75 cr.

The data in respect of Pension Fund as of March 2017 the data is not yet released as the meeting of the Trustees of the Pension Fund is yet to be convened.

- OUR BANK:

The financial results of our bank for the quarter ended June 30, 2017 is as under:

Global Business grew by 10.5 per cent to 670971 crore as on June 30, 2017 from 607280 crore as on June 30, 2016

The total deposit of the bank grew from 338727 crore as on June 30, 2016 to 375796 crore as on June 30, 2017 showing growth of 10.9 per cent. CASA deposits grew by 25.1 per cent to 133412 crore as on June 30, 2017 from 106604 crore as on June 30, 2016. CASA share in total deposits improved to 35.5% as on 30 June, 2017 compared to 31.5 per cent as on June 30, 2016. Savings Deposit registered YoY growth of 27.6 per cent.

Bank’s global Advances grew by 9.9 per cent (YoY) to 295175 crore as on June 30, 2017 from 268553 crore as on June 30, 2016. Domestic Advances increased by 9.4 from 242935 crore as on June 30, 2016, to 265683 crore as on June 30, 2017.

Gross NPAs stood at 12.63 per cent as on June 30, 2017 as against 11.17% as on March 31, 2017 and 10.16% as on June 30, 2016. Net NPA ratio stood at 7.47 as on June 30, 2017 as against 6.57% as on March 31, 2017 and 6.16% as on June 30, 2016. Provision Coverage Ratio stood at 51.13% as on June 30, 2017 as against 51.41% as on March 31, 2017. It was 49.99% as on June 30, 2016.

Net profit for April - June 2017 increased to Rs. 117 crore from Rs. 109 crore in January – March 2017. The Net Profit for the year ended 31/03/2017 was Rs. 556.00 crore.

Capital Adequacy ratio of the Bank under Basel III is 12.01% as on June 30, 2017 as against 11.79 per cent as on March 31, 2017 and 10.75 per cent as on June 30, 2016 compared to minimum regulatory requirement of 10.25 per cent.

The bank has been pioneer in taking various digital initiatives and continuously launched various digital products for enhancing the customer services.

The Bank has 4286 branches as on June 30, 2017 including 4 overseas branches at Hong Kong, DIFC (Dubai), Antwerp (Belgium) and Sydney (Australia). In addition, the Bank has representative offices at Shanghai, Beijing and Abu Dhabi. Total number of ATMs stood at 7575 including 1685 talking ATMs as of June 30, 2017.

Shri. Rajkiran Rai G assumed charge as Managing Director & C E O of our Bank on 1st July 2017. Prior to his elevation as Managing Director & C E O he was Executive Director of Oriental Bank of Commerce. He is an agricultural science graduate and also a certified member of Indian Institute of Bankers. He started his career in 1986 as an Agricultural Finance Officer in Central Bank of India and his rich experience of heading various branches at different parts of the country. On his elevation as General Manager, he was given the responsibility of heading Human Resources Development department.

He was also serving on the Board of Canara HSBC Oriental Bank of Commerce Life Insurance Co. Ltd.

AIUBRF extended a warm welcome to him on taking over as Managing Director & C E O of Union Bank of India.

- ALL INDIA BANK RETIREES’ FEDERATION – OUR NATIONAL ORGANIZATION:

The first convention of the Bank retirees all over India was held at Ahmedabad on 30th April 1994 in which it was resolved to form one united independent apex body of all bank retirees in the country named “All India Bank Retirees’ Federation”.

For the last 24 years, AIBRF has been organizing the retirees in various banks with an object to protect and promote the interest and welfare of retied bank employees across the country. Presently, All India Bank Retirees’ Federation has 52 affiliates comprising of 20 public sector banks, 12 private sector banks, 2 foreign banks, 05 local associations/bodies and 13 State federations. The total membership of AIBRF has now crossed 1,65,000 and more and more bank wise retirees’ organizations are showing faith in AIBRF and seeking affiliation. AIBRF has thus emerged as very vibrant and active organization of bank retirees.

No demand of retirees was conceded by IBA/Government in the last bipartite settlement. AIBRF has committed to take all organizational and legal steps to resolve the long pending demands of the bank retirees. Towards this goal, AIBRF has drawn the following action plan:

- Continue to work to develop cordiality in the relationship with the serving unions without sacrificing its independence and respect;

- Will continue to work for developing coordination among various retiree organizations functioning at apex level in banking industry as well as with other retiree organization in the financial sector;

- To continue to organize Action programmes at different centers to press our demands;

- To organize centralized Dharna cum demonstration at various important centers;

Since then, the AIBRF has carried out the action programmes in order to attract the attention of the government/IBA and also the public at large. AIBRF will take all organizational actions/programmes to pursue retirees’ demands and legal option on selective basis.

- CHARTER OF DEMANDS SUBMITTED BY A I B R F:

AIBRF has released the Charter of Demands on retirees’ pending issues to be pursued during the present wage settlement.

AIBRF also handed over the document of Charter of Demands to UFBU on 1st July 2017. The UFBU Convener has pointed out that the demands of the retirees are already included in the Charter of Demands of workman unions as well as by officers’ Associations and submitted to IBA. UFBU also informed AIBRF leadership their plan to take up the retiree issues effectively during the negotiation and at the same time AIBRF should continue to take steps for creating regular coordination with IBA, Government authorities and constituents of UFBU and also take steps for action programmes at appropriate time to achieve the pending demands. UFBU assured that efforts will also be made for separate allocation of funds for retirees’ demands.

The summary of Charter of Demands is as under:

- Mandate to hold discussion with the retirees.

- Commitments made in the Record Note dated 25/05/2015 should be immediately approved and implemented.

- Grant of 100% DA relief to pre-Nov 2002 retired employees.

- Improvement in Family Pension.

- Updation of Pension

- Pension option to compulsorily retired & resigned employees and left overs.

- Special allowance to be reckoned for superannuation benefits including pension benefits.

- Group Medical Insurance Scheme for retired employees.

- Welfare Scheme for retired employees.

- Issues of Associate Banks, Private Banks, Foreign Banks and RRBs.

- Grievance Cell Setup for retired employees in Banks.

- Management of Pension Fund.

- Improvement in ex-gratia amount payable to those retired prior to 1986 and their spouses

.

The complete text of the Charter of Demands is annexed to this report for information and record of the central committee members.

- 100 % D.A. CASE IN SUPREME COURT: Developments in SLP in the matter of 100 per cent DA case in Supreme Court.

The above SLP of United Bank came for hearing on 01.08.2017 before the honourable bench of the Justice Adarsh Goyal and Justice U. Lalit for leading the arguments.

Senior Counsel of United Bank of India presented in details about the various factors / points on which Division Bench of Madras High Court upheld SLP of the bank managements and details as to how bipartite settlements are held and how allocations of funds are made to meet cost of the settlements. He pointed out that judgement of Madras High Court which is already confirmed by the Supreme Court has dismissed SLP of the retirees.

Thereafter, AIBRF’s Senior Counsel Shri. V.K. Bali initiated arguments on behalf of AIBRF and United Bank of Retired Employees Association. During the arguments, he mainly brought the following important facts before the honourable bench.

(a) AIBRF and bank retirees respect settlement dated 02.06.2005 introducing improved DA formula. Clause 7(2) of the settlement gives details of the improved DA formula.

(b) The above clause of the settlement does not create division among the pensioners based on the date of retirement.

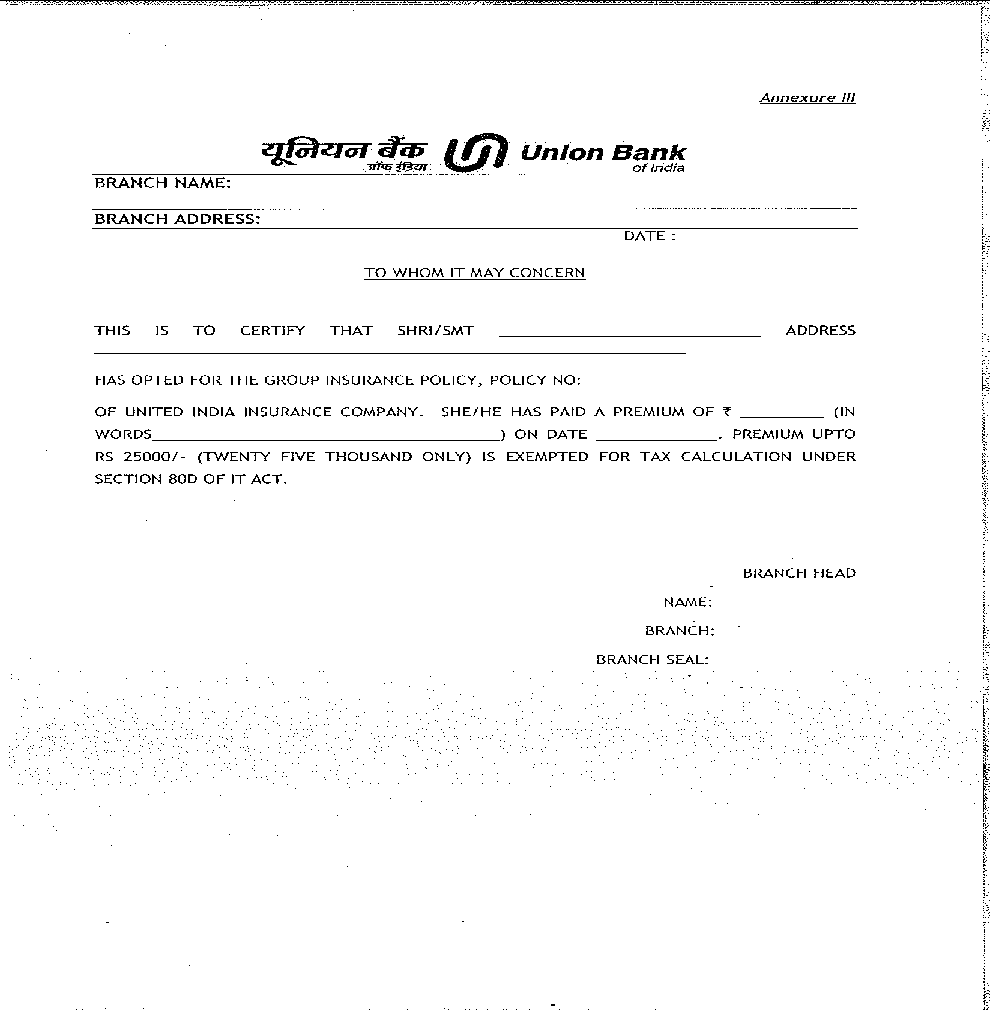

(c) IBA circular dated 28.06.2005 Annexure III which created separate division among pensioners for the purpose of DA payment is only administrative instruction and not settlement in itself.

(d) He also brought to the notice of the Bench that division bench of Madras High Court has committed error in treating IBA administrative circular of 28.06.2005 as part of the settlement. Therefore Madras High Court judgment is based on erroneous facts.

(e) He also made reference of Delhi High Court decision in the matter of LIC and the points which are in favour of retirees.

(g) He also made submission that logically also it looks illogical that senior retirees who need more money get DA at lower rates while new retirees are paid DA at higher rates.

Further another Senior Counsel engaged by AIBRF Shri. Jitender Prasad Sharma submitted before the bench that clause no. 6 of settlement of 1993 on pension scheme is binding on the parties to the settlement until modified or revoked. Therefore DA should be paid as per provision of clause No 6 of 1993 settlement.

In view of the above submissions of two senior counsels of AIBRF, the Bench has agreed to examine the above submissions.

The case was again heard on 23/08/2017. Though AIBRF/ United Bank of India Retired Employees Welfare Association, Kolkata was not direct party in these SLPs, but considering the fact that they were restored by the court in view of new facts brought out by AIBRF’s advocate during the proceedings on 01.08.2017 in the matter of Kolkata High Court judgement and outcome of the above SLPs will have direct bearing on the judgement reserved, AIBRF made request to advocate Shri. V.K.Bali to appear and seek Court permission to intervene in the matter to place record in straight, if required.

Shri V. K. Bali, advocate of AIBRF was asked by the bench to assist the Court in placing the relevant facts of 1 August 2017 proceedings once again.

We understand that the Bank Managements / IBA advocates during the arguments mainly harped on cost factor and pointed out that cost arrears might be quite large say Rs. 4000 crores. On hearing this, the Hon’ble Court has asked IBA / Retirees to submit cost details within one week for the consideration of the Court. The entire proceedings lasted for about 70 minutes. Thereafter the judgements on the SLPs were reserved. and expected to be delivered shortly.

The arguments lead by our counsels in very forceful manner has gone well before the bench and a decision favourable to the retirees was expected.

Further, AIBRF has earlier filed the case as industrial dispute in the matter of 100 % Dearness Allowance with the Deputy Labour Commissioner (Central) Mumbai on 05.12.2016. The conciliation proceedings were held on 24/01/2017 and 28/02/2017 in Mumbai.

AIBRF has moved the case to the Deputy Labour Commissioner (Central) to instruct IBA to hold the negotiations / discussions on the matter of 100% DA as also on other issues of the retired bank employees. The conciliation proceedings are incomplete as the Deputy Labour Commissioner (Central) desired time to study the representations by AIBRF and IBA. The next date of conciliation is not fixed.

The members should note that the role of Deputy Labour Commissioner (Central) is to bring both the parties together for amicable settlement of the issue and if not, the said authority will submit the “failure” report to the Labour Ministry for further action.

AIUBRF appreciates that AIBRF leadership is taking all possible steps to protect interest of retirees.

- IMPROVEMENT IN FAMILY PENSION:

In banks, on death of the pensioners, family pension is paid at the rate of 15 per cent of last pay drawn while in government sector it is 30 per cent of last pay drawn. RBI has also enhanced family pension to 30 per cent for its pensioners. Because of very low ratio of family pension in the Banking Industry, amount of family pension comes down to almost one third of the normal pension on the death of the pensioner. It becomes highly difficult for the spouses who happen to be ladies, in 98 per cent cases, to manage the life. Therefore AIBRF have been pleading with IBA/ Government to increase at par with the government sector / RBI to ensure dignified life to the family after death of pensioners.

- UPDATION OF BASIC PENSION TO PAST RETIREES:

Pension scheme in the banking industry on the lines of pension scheme applicable to the central government employees was introduced in the year 1995. More than 20 years have gone since introduction of pension scheme in banks. During this period 5 wage settlements have been signed giving good increase to the employees in their emoluments. Periodical increase in salaries during last 5 settlements has given increase in pension also to those employees who retired after the settlements. But no increase in basic pension has been considered for the past retirees while signing the wage settlements for employees during last 20 year

This situation has created huge gap in the pension of those retired 10 years or more before and those retiring now. In some case the gap is more than 3 times. AIBRF has been representing to the government and IBA for quite some time that Updation exercise need to be carried out for bank pensioners to draw fair and just balancing and fine tuning between pensions of those retired in the past those retiring now.

AIBRF is pursuing this important issue with the authorities in MoF and IBA. The memorandums were also given to few of the sitting Ministers, MPs and the officials of DFS urging upon them to request the MoF and IBA to consider this legitimate demand of the retired employees. This demand also finds a place in the Charter of Demands of AIBRF.

- PENSION OPTION TO LEFT OVER RETIREES:

Banks had given one more pension option to the left over employees and past retirees in the year 2010 to enable them to join the pension scheme since they could not exercise pension option originally in the year 1995. Today almost 98 per cent of bank employees and retirees are the pensioners. But while implementing the pension scheme in 2010, banks did not allow pension option to two categories of past retirees (a) Resigned and (b) Compulsorily Retired employees. AIBRF want that pension option should be given to the left over retirees whose number is very small to provide them time tested social security at the advancing age of life.

- IBA MUST HOLD DISCUSSION WITH AIBRF:

Indian Bank Association has been refusing to hold discussion/ consultation on retiree issues with AIBRF which represent more than 1.65 lakhs retirees in the name of specific mandate from bank managements. AIBRF wants that periodical discussion should be held with the retirees to ensure speedy disposal of retiree grievances and to create harmonious and cordial relationship with the fast growing community of bank retirees.

AIBRF is requesting IBA to invite AIBRF for discussions / negotiations on the demands / issues of retired employees. But on every occasion IBA informed AIBRF that it is voluntary organisation and render its services based on mandate received from its member banks. IBA also clarified that at present, IBA does not have mandate to hold discussion with the retirees. Therefore it is unable to consider the request of AIBRF in this regard.

In view of the above stand taken by IBA, AIBRF had advised all its affiliates to submit the letter to CMD, EDs and directors of individual banks urging upon them to give mandate to IBA to invite AIBRF to hold negotiations on the retirees demand in the ensuing wage settlement.

AIUBRF had submitted the letter to the management and received the reply stating that our Bank has not received any communication from IBA/Government that they are going to discuss/negotiate with Retirees as part of the current Bipartite Settlement talks nor they (IBA Government) have sent any communication seeking mandate from the Bank to invite AIBRF for discussion/negotiations on retired employees demands/issues.

- Pension related issues - Improvements in Pension Scheme similar to RBI/Central Government including for past retirees - Extension of erstwhile Pension Scheme in banks in lieu of NPS - Follow-up of Record Note dated 25.05.2015

Pension Scheme was introduced in banks on the lines of government/RBI scheme. While improvements have been made in their scheme, the same are being denied in the banks. Other demands raised by AIBRF/UFBU for updation of pension, improvement in family pension, uniform DA for past retirees, etc. were discussed and a record note was signed on 25-5-2015. But two years are over and there is delay in discussing the issues further. There is also a demand of UFBU to extend DA linked pension scheme for employees recruited after 1-4-2010.

AIBRF sincerely expects that UFBU leadership will pursue the demand for settlement on the points in Record Note in the present Bipartite Negotiations for the betterment of the retirees.

AIUBRF is confident that AIBRF and UFBU combine will make all efforts and follow up to secure the long pending demands of the retired employees; and will also initiate further appropriate steps to take the issues forward.

- 11th BIPARTITE SETTLEMENT:

Negotiations for wage revision for employees and officers has already commenced. To facilitate expeditious discussions on Charter of Demands, IBA has constituted separate Sub Committees.

IBA has agreed to the demand of UFBU that the settlement to be effective from 1st Nov. 2017.

In the meeting of 02/08/2017 with IBA, UFBU emphasized the need to hold a round of discussions to follow up the issues covered by the Record Note signed on 25-5-2015 on demands like periodical updation of pension, improvement in Family Pension, 100% DA on pension to past retirees, etc. and we understand that IBA has agreed to discuss the same.

The wage negotiations are continuing since July 2017 and the last meeting was held on 23/08/2017. In this meeting IBA proposed introduction of the concept of Cost to Company package, need for Fixed-cum-Variable Pay and performance related wages to recognize efficiency and performance of employees, rationalization of Special Pay posts etc. UFBU did not agree to some of the above proposals and in some matters requested for additional information / data from IBA.

UFBU also placed the demands as contained in the Charter of Demands for improvement in service conditions. It is reported that meaningful discussions took place on these issues during the round of negotiations. The parties agreed to continue the discussions further in the full Negotiating Committee meeting since the issues are common for employees and officers; and accordingly the next meeting is fixed on 6th September 2017.

In this situation, All India Bank Retirees’ Federation has approached UFBU leaders and submitted the retirees’ issues to them, while requesting them to ensure redressal by IBA. Since UFBU has already taken up the issues of Record Note of 25/05/2015 with IBA during negotiations, let us be positive that the issues mentioned in the Record Note will be clinched.

UNION BANK OF INDIA RETIRED EMPLOYEES’ MEDICAL ASSISTANCE SCHEME (UBIREMAS):

The subject Scheme for the retired employees is in place since 1st January 2003. Initially, the ceiling on reimbursement of hospitalization expenses was upto Rs. 50,000/- for the family (self and spouse), and increased periodically to Rs.125,000/-. In the meeting of the Staff Welfare Committee of our Bank held on 16th and 21st December 2016, the quantum of reimbursement of hospitalization was increased to Rs. 1,50,000.00 w.e.f. 01/01/2017.

This In-house medical reimbursement scheme is a beneficial scheme for the retired employees; but it was observed that many retired employees were unaware of the UBIREMAS and did not join the scheme; thus being deprived of the benefits. AIUBRF followed up persistently with the bank management and also persuaded members of the Staff Welfare Committee to reconsider and to give one more opportunity to those who could not become member of the Scheme earlier, to opt for the scheme. The Staff Welfare Committee agreed to reopen the scheme in 2015. But it was disappointing to note that the number of new enrolments was very low. It is also surprising to note that some recently retired employees too have not become members of the scheme.

As proposed in the forums of AIUBRF, we are persuading the Staff Welfare Committee (SWC) and Bank management to enhance the quantum of reimbursement of hospitalization and also increase the reimbursement of diagnostic check-up from Rs. 2000/- to Rs. 5000/-. But the same was not acceded in the last SWC meeting, and our demand is still pending with the SWC. But, the SWC agreed to subsidise the Insurance premium of widows of retirees getting less than Rs.10,000 pension from the fund upto 50% of the premium. We understand more than 200 retirees’ spouses have benefitted from this subsidy.

All of you are aware that as per guidelines issued by the government, our bank is providing funds to the extent of 3% of the Net profit or Rs. 25.00 Crore whichever is less, every year for the Welfare Measurers for the employees including retired employees. Our Bank has been providing full allocation of Rs. 25 Cr towards Staff Welfare Measures for the last several years and accordingly Bank has been extending various staff welfare schemes to its entire workforce and also the retired employees. Our Bank has the distinction of the “Profit Making Bank since its inception” and the quantum of profits earned during the period also ensured allocation of maximum permissible quantum for staff welfare measures.

However for the year ended 2016-17 the Bank made a net profit of Rs 556 cr in the most difficult circumstances. As such it could provide only Rs. 16.68 crore, being the 3% of the net Profit, towards the Staff welfare Measures as per guidelines in vogue.

We need to understand that this lesser allocation will definitely result in curtailment of budget of the staff welfare measures, and the same may lead to pruning of various staff welfare schemes or to discontinuation of some schemes. We need to await the outcome in the near future of SWC continuing all the schemes including UBIREMAS with the same budget allocation as it is, provided the Bank allocates the same amount as has been done in the previous years.

We understand that Com. N. Shankar, the General Secretary of AIUBEA, and a member of the Staff Welfare Committee has requested the Bank management to allocate the full allocation of Rs. 25 cr for Welfare Fund to ensure continuance of all the schemes.

In the background of the provision of reduced amount of Welfare Fund as explained hereinabove, we have to realise that the demands for increase in quantum of hospitalization, reimbursement of diagnostic tests etc., may not be financially feasible. We request central committee members to deliberate on this important subject keeping in mind the above facts, and to arrive at pragmatic conclusions to enable AIUBRF to list demands to the bank management and Staff Welfare Committee on UBIREMAS.

DEMAND FOR SUBSIDY FOR PART PAYMENT OF PREMIUM AMOUNT OF MEDIAL INSURANCE SCHEME:

AIUBRF had requested the Bank to consider subsidizing the part of the enhanced premium amount payable under the Medical Insurance Scheme from the funds of UBIREMAS for retirees, as has been done by several Banks.

However, the management argued that premium amount could not be subsidized from funds of UBIREMAS because many of the retirees who opted for the Medical Insurance Scheme are not members of UBIREMAS and vis-a-versa. The management further clarified that if the premium amount is subsidized, UBIREMAS scheme needs to be closed due to which additional hospitalization of Rs. 1,25,000/- and now Rs. 1,50,000/- would not be available to the members of UBIREMAS.

Persistent follow up with the management and the timely intervention of Shri. N. Shankar, member of Staff Welfare Committee of our Bank, it was decided by the bank to extend 50% of insurance premium on medical insurance scheme as subsidy to family pensioners who are drawing family pension upto Rs. 10,000/- per month for the year 2016-17. An amount of Rs. 34.00 approx. was reimbursed to the family members.

AIUBRF is still receiving letters/requests from members to demand for subsidizing the part of the insurance premium. But in view of the reduced allocation of Welfare Fund to Rs. 16.88 crore against Rs. 25.00 Crore for this financial year, the demand for subsidy may not find positive response from the bank management. We have discussed the financial budgetary aspects with some members of the SWC, and have pointed out how availability of some amounts in the budget could be utilized to find a way out for subsidy for retirees.

AIUBRF does not wish to brush aside the demand of subsidy, but would like the central committee members to debate on the issue to come to some understanding of the situation and circumstances prevalent now and take informed decision in the matter.

- MEDICAL INSURANCE SCHEME OF IBA/BANK FOR RETIREES:

IBA has introduced Medical Insurance Scheme since Oct / Nov 2015.

The group medical insurance scheme has salient advantages like availability of insurance cover to all retirees irrespective of age, coverage of pre-existing ailments and provision of reimbursement of domiciliary expenses.

Majority retired employees joined the Medical Insurance Scheme in view of above mentioned important benefits as well as the amount of premiums payable by the retired officers and award staff, were moderate and less than the premium amount payable for individual medi-claim insurance policies of other general insurance companies.

In September, 2016 the bank informed the retired employees about the likely increase in the premium amount for the renewal of Group Insurance Policy for the year 2016-17. AIUBRF wrote a letter to the management expressing strong objection to the steep increase in the premium amounts likely to be deducted, within a period of one year of commencement of insurance policy.

Consequent to our letter, the bank management convened a meeting of office-bearers of AIUBRF with the executives of the personnel department. In the meeting, AIUBRF protested to the Bank Management that members were opposed to any unilateral or exorbitant increase in Insurance premium amount by UIIC/IBA for retirees, as proposed for existing employees.

The management informed AIUBRF that the premium payable by the retired employees / officers was hiked by UIIC since the claim settlement ratio was at a high of 230%. AIUBRF pointed out that retirees are paying the premium themselves and hence the burden should not be too much for them. Further we also pointed out that domiciliary treatment expenses were not being reimbursed for the retirees in the scheme at that point of time.

AIUBRF leadership was able to interact and get a sense of the realities involved. There was a danger of retirees losing out completely if UIIC continued its adamant posture on the premium increase, and/or renewal of the policy. AIUBRF, therefore, requested the Bank not to take immediate action on any unwitting withdrawal by any retiree, without knowing all the facts or information of such proposed premium deduction from the pension accounts.

In the meantime, AIUBRF advised members to send protest letters, which reflected the fighting spirit of the retirees of Union Bank.

Though the negotiations / discussions on steep increase in premium amount were going on between banks/IBA and UIIC, the payment of renewal of policy was falling due on 31/10/2016. In order to avoid any adverse effect by non-payment of renewal premium, 18 banks had paid the premium amount on behalf of their employees. This had caused pressure on other banks which were waiting for the outcome of the discussion with UIIC. But subsequently these banks also paid the increased renewal premium to UIIC.

In the backdrop of the above developments, AIUBRF had taken an informed decision to protect the interest of retirees by advising them to continue the cover of the insurance policy because other private players might not extend the same features already explained earlier.

AIUBRF therefore requested the management to reduce the burden of retirees to manage the funds by crediting the monthly pension before 24/10/2016, and extend a loan facility to the needy retirees to meet the enhanced premium amount, and permit them to submit their option letters a fresh till the last date of payment of premium amount. Due to the swift action undertaken by the leadership of AIUBRF, we could get a positive response from the management on the above matters, thereby agreeing to all our above suggestions.

One of the subsequent improvements in the renewed insurance policy was that UIIC agreed to reimburse domiciliary expenses to the extent of Rs. 40,000/- for officers and Rs. 30,000/- for award staff within the insurance cover of Rs. 4.00 lakhs and Rs. 3.00 lakhs respectively with payment of an additional amount.

Following are the number of retirees who opted for the Group Medical Insurance Policy for the period 2016-2017.

Type of Insurance Policy

|

Officers

|

Award staff

|

Total

|

Without domiciliary benefit

|

4236

|

2599

|

6835

|

With domiciliary benefit

|

3596

|

1289

|

4885

|

Total

|

7832

|

3888

|

11720

|

There are very many inquiries from the members in respect of submission of hospitalization / domiciliary claim and deficiency letter by TPA etc. We have at the end of this report attached the gist of the Insurance Scheme which will be useful to properly understand the insurance scheme.

The existing insurance policy of UIIC is due for renewal on 31/10/2017. The claim ratio for 2016-17 in respect of the retirees is 126% under non-domiciliary category and 201% under domiciliary category. If clubbed as had been done last year, the overall ratio will be within 120%. But, if retirees are separated from in service employees, the loading of premium for retirees will be very high and beyond the reach of retirees. This may force many retired employees to exit from the scheme; and in the long run, it is feared that the scheme will be rendered out of bounds of retirees, which may result in discontinuance of the scheme.

Hence, in order to quantify the likely insurance premium amount for the period from 01/11/2017 to 31/10/2018, we requested our Tamilnadu Unit to approach the officials of UIIC at Head Office at Chennai to get their views on the matter.

Shri. K. R. Ravi, Jt. General Secretary of AIUBRF and General Secretary of our Tamilnadu Unit had met the top management personnel of UIIC and the following information emerged:

- UIIC has so far not sent offer letter to the Indian Banks Association in respect of proposed amount of premiums for the retired employees.

- The claim ratio in respect of policy without domiciliary benefit is around 126%.

- UIIC is inclined to quote the existing premium rate for the insurance policy without domiciliary benefit.

- The claim ratio of Insurance policy with domiciliary benefit is about 201%.

- UIIC is contemplating to increase the insurance premium of policy with domiciliary benefit by 25% over the existing amount of premium Rs. 20,010.00.

On receiving the above feed-back from our Tamilnadu Unit, AIUBRF has written a letter to AIBRF to take up the issue at the appropriate forum and also inform IBA to firmly negotiate with UIIC to ensure there is no increase in the insurance premium as contemplated.

We understand the matter of future rate of the insurance premium for retired employees has not come up for discussion in the last three meetings of UFBU and IBA; all efforts are being made to ensure undue increase of premium of the insurance policy for retired employees, falling due after 31/10/2017, is not unduly increased. We expect that UFBU would take up issue for discussion in the next meeting with IBA.

We understand that recently IBA has informed the banks that based on the anticipated Incurred Claim Ratio (ICR) of around 107% of the existing employees for the full year; United India Ins. Co. confirmed that the policy can be renewed for the next year (1-10-2017 to 30-9-2018) on the existing premium rates without any increase. Hence IBA has advised all the Banks to remit the premium as per last year and renew the policy.

Considering the decision of UIIC to continue the rate of premium at existing level for employees, the retired employees too may expect the same rate of premium be fixed for the next year i.e. 2017-2018, except for those who have availed domiciliary policy. This could be increased marginally.

We request central committee members to deliberate on this very important issue and decide the future line of action to educate the retired employees whether to continue with the scheme or not.

SUPER TOP UP MEDIAL INSURANCE POLICY DESIGNED BY NEW INDIA ASSURANCE COMPANY FOR BANK RETIREES:

As stated in preceding para, Indian Bank Association had introduced Group Medical Insurance Policy designed by United India Insurance Company for bank retirees with effect from 1st November, 2015.

In the existing medical insurance scheme there is no provision for top up facility for the retirees which is common option given to the insured by the insurance companies to meet individual needs. At the time of last renewal of the medical insurance policy AIBRF had approached IBA to consider providing option of Top Up facility; but IBA did not respond.

Since then, AIBRF was considering that some reliable option at reasonable and affordable cost should be available to the retirees for buying super top up insurance policy in addition to the basic policy of United India Insurance Co. to meet growing expenses on medical treatment and to avoid risk of not getting additional cover at the later stage in view of advancing age. AIBRF has put in all efforts in this regard by contacting IBA and UFBU for introduction of super top up scheme for retirees but received no positive response.

It may kindly be noted that only after the launch of Super Top Up policy by AIBRF and New India Assurance Company in the month of July 2017, M/s. K.M Dastur Reinsurance Brokers Pvt. Ltd., of UIIC circulated letter of intent to the constituent of UFBU informing their desire to introduce the Top Up policy for the retired employees. Immediately, AIBRF has written letter to UFBU to ascertain whether they will support for the approval by IBA. However no response was received from UFBU. Likewise, IBA too did not respond to the letter of AIBRF in this regard.

Since no response was forthcoming either from IBA or UFBU, AIBRF took initiative to launch independent insurance scheme for additional cover to ensure welfare of members of AIBRF.

AIBRF has finalized the terms and conditions of the Top Up policy with the New India Insurance Company, which is also the unit of the public sector insurance companies. The Top up policy designed for bank retirees will have 100 per cent same terms and conditions and will be completely identical to the basic policy of UIIC.

Following are the salient features of the Top Up Scheme finalized by AIBRF with New India Assurance Co.

- Retired employees who are members of medical insurance scheme of United India Insurance Co. Ltd and opt for renewal for 2017-2018 will be eligible to apply for this Super Top Policy.

- Sum Insured under this scheme will be Rs. 3 lakhs for award staff and Rs. 4 lakhs for officer staff.

- Annual Premium will be as under

For Rs. 3 lakhs Rs. 3511 (inclusive of GST)

For Rs. 4 lakhs Rs..3806 (inclusive of GST)

- This policy will be effective from 1st November 2017 to 31st October, 2018.

- Those who desire to buy this Super Top Policy should submit the request in the proposal form duly filled in.

- Cheque should be in favour of “ AIBRF New India Super Top up Policy”

- Policy will cover only hospitalization charges with 30 days pre-hospitalization and 90 days post hospitalization expenses on the lines of basic policy. Domiciliary benefits will not be available under top up policy.

- The policy will become operative from 1st November, 2017 to coincide with due date for next renewal for basic policy subject to getting minimum 10000 applications with premium payment before the due date .

As informed in this topic earlier, M/s. K. M. Dastur Reinsurance Brokers Pvt. Ltd., wrote a letter to UFBU constituents informing that UIIC, in spite of the losses, have agreed to give Super Top Up cover i.e. an additional healthcare cover for the Retirees, looking at the Incurred Claim Ratios which are 126% for the Retirees Policy without Domiciliary cover and 201% for Retirees with Domiciliary Cover as of 16th July 2017.

United India Insurance Co. Ltd has confirmed to issue a Super Top Up Policy for the Retirees as per the terms and conditions of the IBA policy for Retirees without the Domiciliary cover.

The procedure for implementation of the Scheme of UIIC is similar to that of the Super top Up policy of New India Assurance Company except the following important features:

- UIIC offers additional insurance coverage (Top Up) of Rs.4 lacs (for retired workmen) & Rs. 5 lacs lakhs (for retired officers) instead of Rs.3 lakhs and Rs.4 lakhs offered by New India Assurance Company.

- The rate of premium proposed for enhanced cover of Rs. 1.00 lakh for retired award staff i.e. (Rs. 4.00 lakhs) and officers (Rs. 5.00 Lakhs) is same as quoted by New India Assurance Company for Super Top Up policy of Rs. 3.00 lakhs and Rs. 4.00 lakhs. The details are given in the table given here under for better understanding:

Sum Insureds of the two New Super Top Up Policies

|

Threshold i.e. the Sum Insured under the main Policy after which the Super Top Up Policy will trigger

|

Premium excluding GST*

| |

Rs.

|

Rs.

|

Rs.

| |

1

|

4,00,000

|

3,00,000

|

2,975*

|

2

|

5,00,000

|

4,00,000

|

3,225*

|

The Third Party Administrators is the same as the ones dealing with the main policy.

In view of the Top Up scheme being introduced by two insurance companies simultaneously, it is now become imperative to debate and decide on how to disseminate both schemes to the members, to enable them to take informed decisions.

The amount of renewal of premium for Insurance Medical Policy for 2017-18 without domiciliary cover, which has a small increase due to the GST, has been conveyed by UIIC to IBA as follows:

Award Staff retiree: Rs.10,452 + 1881 GST @ 18% = Rs.12,333

Officer retiree : Rs.13,935 + 2508 GST @ 18% = Rs.16,443

Premium for Insurance Policy with domiciliary benefit is yet to be declared.

Similarly, the premium for Top Up policy by UIIC/IBA, has not been officially intimated by IBA and members need to know the same, to ensure informed decision when opting for the top up policy best suited to them.

Only if the UIIC top up is NOT forthcoming by IBA, AIUBRF may advise members to decide about opting for the Top Up policy of New India Assurance Company.

We request the central committee members to discuss the issue threadbare and take the informed decision to enable AIUBRF to advise the membership accordingly.

ISSUES PERTAINING TO EXERCISE OF OPTION FOR DOMICILIARY BENEFITS UNDER THE MEDICAL INSURANCE SCHEME:

IBA/UIIC introduced the scheme of domiciliary benefits within the sum insured @ 10% of Rs. 3.00 lakhs for award staff and Rs. 4.00 lakhs for officers; by payment of additional premium by the retired employees.

Our Bank accordingly instructed the branches to inform all the retired employees drawing pension from their branches about the new feature under the medical insurance scheme. AIUBRF as well as all the state Units had also taken the steps to inform their membership about the facility of reimbursement of domiciliary treatment and appealed them to opt for the insurance cover with domiciliary benefits. However, due to steep increase in the premium amount for the period 2016-2017, few of the retirees did not join the scheme. We have provided the details of the number of retirees opted for insurance policy with and without domiciliary benefits.

Our bank had instructed all the retirees to submit the option letters “on line” for opting medical insurance scheme with or without domiciliary benefits. The option letters were to be sent to Central Office directly for which a dedicated email address was provided. Many of the retired employees exercised their options by following the guidelines of the bank for submission of option letters.

But in few cases it was noticed that the option letters submitted by the retired employees either through their pension paying branches or directly were reportedly not received at Central Office due to which the premium amount for availing domiciliary benefits was not recovered; thus they were deprived of the facility. AIUBRF leadership stationed at Mumbai took the task of informing the bank about the correct recovery of premium amount and ensured that such corrections were made. This exercise was continued till middle of December 2016 i.e. for 6 weeks and more than 250 cases had been rectified.

As said hereinabove, few cases remained unattended by the management though these retirees had given option letters for domiciliary benefits within the time stipulated for submission. AIUBRF had taken up such cases with the management but UIIC refused to rectify after 15/12/2016 stating that more time had elapsed since 26th / 28th October 2016 i.e. debit to the accounts.

Since the insurance policy will be due for renewal on 31/10/2017; rectification of pending cases may not be possible within the remaining 7 weeks of the insurance validity. But AIUBRF can take up the issue with the management to allow such retired employees to opt for domiciliary benefits who can submit satisfactory evidence of submitting the option letter within time and/or any acknowledgement thereof can be produced for verification.

SERVICES OF THIRD PARTY ADMINISTATOR (TPA) – M/S. PARAMOUNT HEALTH SERVICES PVT. LTD:

It has been observed that at many centers the representative offices of TPA are delaying sanction the claims of reimbursements. The letters of Deficiency are also not sent to the claimants in time causing delay for sanction of claims. Similarly cases of delay & such like problems are being faced by the in-service employees also.

AIUBRF leadership at Mumbai had arranged a meeting with the General Manager and the senior CRMs of TPA to understand the procedure for receipt of claims, its scrutiny, processing, approval and final submission to UIIC for payment. The officials of TPA assured AIUBRF that efforts are made to ensure the claims are settled expeditiously wherever claim documents are proper & in order, and for the others within reasonable time.

Yet, there are cases of denial of claim & complaints that no intimation is sent or no information/reasons are given for reducing the amount of claim. On taking up the matter with TPA officials it was clarified by them that such information is sent via email, and if no email address is provided, the reasons are intimated to the bank.

By and large, there is general feeling that TPA’s services are far from satisfactory.

AIUBRF had also taken up the matter with the bank management with a request to take up the issues with TPA for improving the services to the retired employees.

We understand a workshop is likely to be conducted on 22nd Sept 17, by AIUBEA with the TPA/ Bank officials, to impart clarifications on the effective working of the scheme in future. We may explore possibility of our retiree representatives also being involved in the same.

FORMATION OF OTHER RETIREES’ ASSOCIATION IN OUR BANK & CO-ORDINATION:

Organizing retired employees was necessitated within 5 years after promulgation of Pension Regulations for the improvement in benefits of the retirees, which included the pension scheme and other related issues.

During the last 16 years, our Federation has been receiving encouraging response from the retirees of our Bank from various States, who have enrolled themselves as affiliates of the Federation. Presently we have 21 Affiliates.

We categorically state that AIUBRF has never indulged in any kind of divisiveness or rivalry against any other Union Bank retirees’ organizations, even though a separate rival outfit was formed by an initiative sponsored by AIBOC & INBOC.

AIUBRF firmly believes that there is no need of another retiree organization in Union Bank, when retirees from all trade unions have formed AIUBRF, despite earlier ideological differences, understanding the relevance of a cohesive, united retiree movement. The AIUBRF was formed in the year 2000, and is an independent organization not having any affiliation with any national organizations or of active service employees. Whereas AIBOC & INBOC retirees organizations have come into existence much later. We have always attempted and will continue to ensure all retirees consolidate under one umbrella i.e. AIUBRF, to ensure a unified approach of all retirees to their issues and towards building a resolute retiree body in the Bank and in Society. To this end we invite all Union Bank retirees to Unite and participate in the functioning of AIUBRF, and ensure a single apex level retirees’ Federation in Union Bank.