The Madras High Court Bench here on Friday dismissed an anticipatory bail application filed by a former bank manager in a case booked against him on the charge of swindling Rs. 1.31 crore by sanctioning bogus loans to self-help group members. Justice P.N. Prakash dismissed the application filed by Mahendran, former manager of Sayalkudi branch of Union Bank of India, on the ground that the nature of allegations levelled against him were very serious and the amount of money involved in the case was also huge.

Though the petitioner accused his successor in the bank branch of having lodged the complaint with ulterior motives and without obtaining the permission of his superiors, the judge said the Code of Criminal Procedure did not make such permission a sine qua non for setting the law in motion.

The judge said a communication sent by the bank’s Regional Office to the complainant, Sesha Mari Kumaran, on February 18 sought his explanation only for not keeping the matter in wraps and allowing the media to get a wind of it thereby causing loss of reputation to the bank’s name.

Complaint

“By lodging such a complaint, even without the permission of the higher-ups, the defacto complainant would have at the most violated some departmental rules, but that cannot in any way make the FIR illegal,” the judge added.

PSU banks to tie-up with insurers for social schemes by June 1-Business Standard

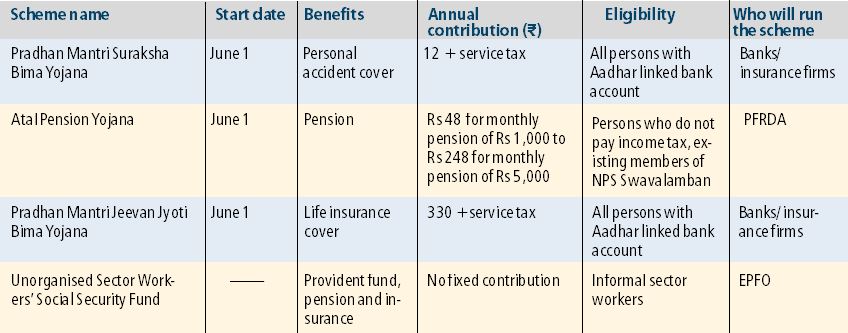

Insurers to offer Rs 2 lakh accident cover for a premium Rs 12 a year and life cover of Rs 2 lakh for an annual premium of Rs 330

After the Pradhan Mantri Jan Dhan Yojana (PMJDY) that had kept the banks busy, it is the insurance schemes (group-term and personal accident) announced in the Union Budget, which are to be offered to all account-holders, that are now in focus. Insurance executives said that in the initial stage, the companies will tie-up with public sector banks first and later with private banks.

Public sector insurers like Life Insurance Corporation of India (LIC) have already tied-up with banks Dena Bank, Corporation Bank and IDBI Bank to implement the Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJBY) for savings bank account holders.

In a recent Indian Banks' Association (IBA) meeting to discuss social security schemes in insurance and pension, all member banks were requested to explore tie-ups with suitable insurance companies who are willing to offer insurance schemes. These schemes would be on terms similar to those offered by LIC and the public sector general insurance companies.

Public sector insurers like Life Insurance Corporation of India (LIC) have already tied-up with banks Dena Bank, Corporation Bank and IDBI Bank to implement the Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJBY) for savings bank account holders.

In a recent Indian Banks' Association (IBA) meeting to discuss social security schemes in insurance and pension, all member banks were requested to explore tie-ups with suitable insurance companies who are willing to offer insurance schemes. These schemes would be on terms similar to those offered by LIC and the public sector general insurance companies.

"As announced in the Budget, we are required to tie up with banks, since there will be direct debit of premium from bank accounts. Discussions are on regarding how to implement the schemes and atleast the public sector insurers (life and non-life) will tie-up with the major PSU banks by June," said a senior public sector insurance executive.

Public sector bank executives said the initial costs are going to be much more than the fee that will be proposed to be paid. Bank staff especially at branch level would have to shoulder burden.

In his budget speech, finance minister Arun Jaitley said that two new insurance schemes for the lower income groups will be launched. He had said that the Suraksha Bima Yojana, an accident insurance scheme of Rs 2 lakh sum assured with premium of just Rs 12 a year, would be launched. Prior to finalisation of terms, insurance companies had indicated premium of Rs 24 to be a proposition viable. But the ministry prevailed to reduce to it to make it more attractive for the masses, said a bank executive.

Similarly, there will be a Jeevan Jyoti Bima Yojana with a life insurance cover of Rs 2 lakh with an annual premium of Rs 330. This will be for those between the age-group of 18 years to 50 years. Jaitley said that these schemes will be part of a Universal Social Security Scheme in the country.

There would also be an Atal Pension Yojana (APY) that will be launched, also to be offered through banks. The modalities of this scheme are being worked out with Pension Fund Regulatory and Development Authority (PFRDA).

APY will be focussed on all citizens in the unorganised sector, who join the National Pension System (NPS) administered by PFRDA and who are not members of any statutory social security scheme. Under the APY, the subscribers would receive the fixed pension starting from Rs 1,000 per month, and in multiples thereof, subject to a ceiling of Rs 5,000 per month, at the age of 60 years. The monthly pension amount would depend on their contributions, which itself would vary on the age of joining the APY.

This scheme is open to all bank account holders who are not members of any statutory social security scheme. All bank account holders under the eligible category can join APY with auto-debit facility to accounts, leading to reduction in contribution collection charges.

Both public and private life and general insurers can participate in these schemes. Industry officials said that this would be similar to the other schemes where a tender will be floated and quotations will be sought. Insurers would require to apply state-wise for getting a particular scheme contract implementation in each state.

In the budget speech, Jaitley said that the premium for this scheme would only be direct debit from the bank accounts and only account-holders would be eligible for the product.

The country's insurance penetration (measured as premium as a percentage of GDP) has fallen to 3.9 per cent in 2013-14 compared to 4.0 per cent in 2012-13. With these schemes, insurers expect the penetration levels to increase. However, this is not a new phenomenon. With lower rates of renewal and lesser disposable income available to invest, insurers said that the penetration has come down.

While the PMJDY was only open to those people who did not have a bank account, these schemes are open to anyone who wishes to be part of the scheme. Further, these schemes would not be subsidised by the government and all claim-related services would be provided by the banks.

Insurers said that they are still in talks on how to deal with individual claims in the life and non-life schemes. Designated bank branches will be set aside for these claims and there would atleast 2-3 personnel in each branch handling these claims. Apart from this, renewal facilities would also be given by banks.

Personal Finance: Social security boost: Range of new pension, insurance schemes on anvil-Indian Express-19.04.2015

A plethora of new schemes for pension and insurance are set to be launched this year by the government with an aim to provide universal social security. Contrary to popular perception, many of these will be available to all citizens and not just to those living close to the poverty line.

The three key schemes include Pradhan Mantri Suraksha Bima Yojana, Atal Pension Yojana and Pradhan Mantri Jeevan Jyoti Bima Yojana that were announced by finance minister Arun Jaitley in the Union Budget 2015-16.

Pointing out that a large proportion of the country’s population is without insurance of any kind, the minister had announced, “Worryingly, as our young population ages, it is also going to be pension-less. Encouraged by the success of the Pradhan Mantri Jan-Dhan Yojana, I propose to work towards creating a universal social security system for all Indians, specially the poor and the under-privileged.”

The finance minister has already held one round of meeting with public sector banks on the launch of these schemes. The plan is to implement these on the same scale as account opening under the Pradhan Mantri Jan-Dhan Yojana. To ensure ease for customers, subscription and claim forms will be kept simple and the finance ministry is also thinking in terms of empowering banks to enable faster claim resolution under these schemes.

Significantly, in the interim, the Employees’ Provident Fund Organisation has also proposed a new social security fund — the Unorganised Sector Workers’ Social Security Fund that can be joined by any private sector worker.

The Indian Express takes a closer look at each of these schemes:

Atal Pension Yojana: A co-contributory fixed pension scheme, the Atal Pension Yojana will be focused at unorganised sector workers who are not members of any social security scheme. The scheme is expected to be launched from June 1, 2015.

Under the APY, subscribers would receive a fixed monthly pension of Rs 1,000; Rs 2,000; Rs 3,000; Rs 4,000 or Rs 5000, depending on his or her contribution, starting from the age of 60 years.

The minimum age for joining the scheme is 18 years and the maximum is 40 years with a minimum contribution period of 20 years. Contributions would vary from as little as Rs 48 a month for a Rs 1,000 pension to Rs 248 a month for a pension of Rs 5,000 per month, according to a finance ministry official.

The Central government would provided a fixed return by co-contributing either 50 per cent of the subscriber’s contribution or Rs 1,000 per year —whichever is lower; for a period of five years from 2015-16 to 2019-20 for subscribers who join the National Pension System before the end of this year.

However, do keep in mind that the Central government contribution would be available only for those subscribers who are not income tax payers. The existing subscribers of the NPS Swavalamban scheme would be migrated to the APY, unless they opt out of it, according to note prepared by the department of financial services in the finance ministry.

The scheme would be administered by the Pension Fund Regulatory and Development Authority and investments would be done on the pattern as that for NPS for central government officers.

No comments:

Post a Comment